General Interest derivatives pricing API framework. And FRAs, Duration, Yield,..

Java Components offering general Interest derivatives pricing framework: set contract and vol/price/interest models and run MC. Including the pricing and risk analytics of interest rate cash and derivative products. We also cover the fundamental theory of bonds including: Treasury bonds, Yield/Pricing, Zero Curve, Forward rates/FRAs, Fixed-Interest bonds, Duration and Convexity. Download then "java -jar *.jar" at prompt.

WebCab Bonds implements the following functionality:

- Fundamental Theory of Bonds

- Pricing and Yield

- Constructing the Zero Rate Curve

- Forward Rates and FRAs

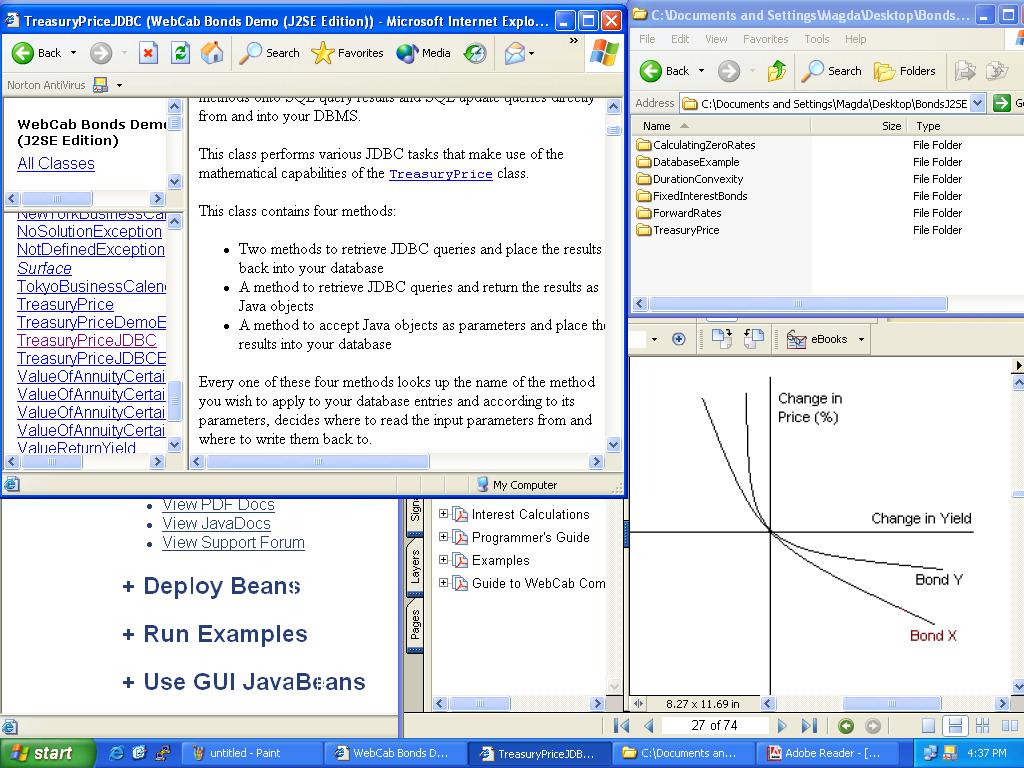

- Duration and Convexity

- Yield of Fixed-Interest Bonds on Interest payment dates

- Interest Calculations

This product also contains the following features:

GUI Bundle - we bundle a suite of graphical user interface JavaBean components allowing the developer to plug-in a wide range of GUI functionality (including charts/graphs) into their client applications.

JDBC Mediator - A J2SE Component which mediates between a J2SE component, its J2SE Clients and the Database server. The JDBC Mediator J2SE classes are a convenient way of enhancing all financial and mathematical specific methods with JDBC-based functionality. Check the jdbc subpackage of every J2SE class for JavaDocs documentation.

Web Application Example - A Java WAR file which contains a JSP example that makes use of the functionality provided by our J2SE Component.

Synthetic JDBC - The JDBC functionality provided by the Web Application example included within this package. This Web Application is an example of how to make a JSP client using our J2SE Component while manually implementing the JDBC code. The JSP Application applies J2SE methods to certain rows from the database and lists the output in HTML format.